Leslie Willcocks

Professor Emeritus

London School of Economics and Political Science

Businesses have been utilising information technologies since the 1960s. Across over 60 years of organisational computing businesses, governmental agencies and others have seen five eras in which new technologies emerged, then were exploited for organisational advantage. The management of information technologies, and the information systems and applications they support has been in constant evolution to keep up with, develop and run emerging technologies. To understand the management challenges a little history is very useful.

Currie, Willcocks and Seddon (2026) discern five eras of computing each focused on developing and operationalising new technologies as they came on stream (see Figure 1). The first three eras we are not needing to go into detail on, but please note that their technologies are still in use in most international businesses today whether mainframe, PC or internet-based. Each computing era has been driven by a different underlying economics. Thus, the system-centric era was driven by Grosch’s law: ‘Computer power increases as the square of the cost’—meaning that a computer that is twice as expensive delivers four times the computing power. The PC-centric era delivered on Moore’s Law that semi-conductor price-performance would double roughly every two years. Meanwhile in the Network-centric era Metcalfe’s Law became central: ‘the cost of a network rises linearly as additional nodes are added, but that value of the network can increase exponentially’.

The period 2006–2020 (see Figure1, Content/Cloud centric era) provided new management challenges. It saw the development of virtual businesses and individualised services, building on the previous era which had constructed an inexpensive, ubiquitous and easy-to-use high bandwidth infrastructure. The focus of the IT industry shifted from specific technological capabilities to software, content and services, and from on-line channels to customer pull, and embedded systems. The industry driver became the economics of information evolving the nearly infinite scale economies of software with the nearly infinite variety of information content. The law of transformation would come into play. A business needed to become more bit as opposed to atom based. Its transformation would be equal to the square of that of the percentage of that industry’s value added that is bit rather than atom based. This meant that superior business value now came from moving from physical to virtual worlds. This would widen industry/organisation differentials—something many studies recorded happening in this period

To add to the picture, in this period we saw the take-off of Web 2.0, social media, smartphones and digital TV. Meanwhile the technological infrastructure, including cloud computing, had evolved to support mass use of devices, allow huge flows of information in multiple forms, and see the Internet being used by over two billion people by 2012—twice the number using it in 2007. Three billion people worldwide used cell phones by 2010. By 2016, half of the world’s population was connected to the internet and as of 2020, that number had risen to 67 percent. These numbers have only increased since. Meanwhile, ITO/BPO outsourcing began to change character, especially from 2016, seeing declining demand for traditional application development, maintenance, mainframe, IT infrastructure, desktop, business process and IT services and a large trend towards digital sourcing of IT and business services.

.png)

At this moment in time, we are some ways into what Currie, Willcocks and Seddon (2026) discern as the Convergence/AI era stretching from 2020 through to 2035. This will see the development and application of at least ten major advanced technologies. Combining this over time with other technical advances will create synergies and support what we call the Law of Combinatorial Innovation, where learning to combining such technologies in new ways will create superior business value and competitive advantage.

This quick history of computing puts you in the position to understand:

- 1. The techno-management problem. Why global information systems management has so many challenges. Not only are IT managers looking after existing systems and infrastructure, they are continually bombarded with updates and emerging technologies that they have to bring into the organisation in a timely manner, merge with a host of existing technologies, make timely technology ‘drop’ and ‘replace’ decisions—all while helping to gain daily business value and competitive advantage. The 2021–2035 period sees international businesses seeking to harness at least ten new major SMAC/BRAIDA technologies then combine them for business advantage. New technologies, new management challenges.

- 2. The techno-economics problem. How the problem arises of trying to amalgamate and gain superior value from different technologies driven by different economics.

- 3. The techno-dependence problem. How investment in computing and digital technologies has been continuous over many decades and has resulted in global infrastructures that now are fundamental to the functioning and future of international businesses, and how difficult it would be to reverse out of this.

- 4. The techno-skills problem. How an organisation is continually searching to build its in-house team to deal with a variety of technologies and maintenance issues arising, while also staffing to build and exploit newer technologies coming on stream.

- 5. The pressure to use external IT labour and services. It is unlikely that any international business today can run itself on internal IT labour. Thus, IT functions also adopt the digitalised flexible organisation model and also the management challenges that brings.

- 6. The AI problem. How an international business may find dealing additionally with the development, operationalisation and exploitation of AI for business value sets challenges that are not likely to be dealt with in a short time frame. The strategic business value of AI, outside the hi-tech companies that produce AI applications and services, may take much longer to arrive than many commentators assume.

The Evolution of IS Management in Businesses

One way of understanding the relevance and evolution of management practices with information and communication, automation and digital/AI technologies is to look at a digital leader, the Development Bank of Singapore—more often called DBS bank. Over 15 years this bank moved from being a traditional financial service to a digital business. In 2010, at the instigation of its CEO Pyush Gupta it undertook a digital transformation journey that continues into the late 2020s. The reality with these technologies so far is that the journey actually never ends because there are always newer versions, newer technologies, and better ways of combining the old and the new. There is also always a lot of managing to do.

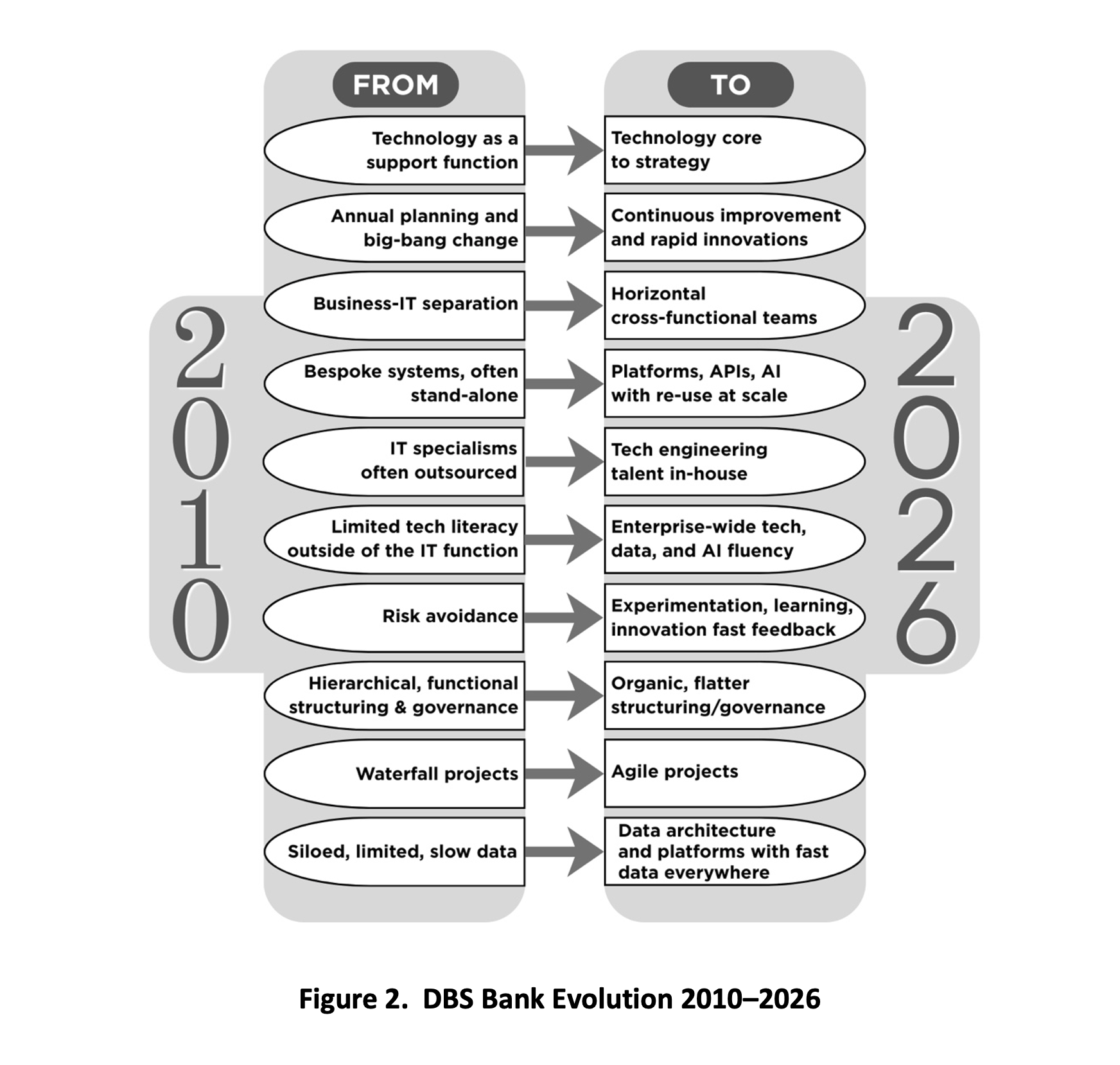

In Figure 2 we show a simplified map of where DBS bank came from, managerially, and what it had grown into by 2026/2027. You will see that the management of technologies has taken on board many of the practices we describe in other chapters—in particular on structuring, human resource management, sourcing, project and change management. This is hardly surprising given the mandate that technology should be aligned with business imperatives, strategy and business operating models.

Understand that DBS bank, as at the mid-2020s and throughout its evolution, has been a relatively uncommon phenomenon, namely a digital leader. Our own evidence (see blog X) suggests that digital leaders constitute only 15–24 percent of organisations, depending on sector. This means that on a conservative estimate nearly 76 percent of businesses are what Willcocks et al., (2024) calls ‘follower’ (trying to replicate), ‘laggard’ (struggling) or ‘nascent’ (very early stages) organisations when it comes to going digital. They find it impractical to replicate DBS bank management practices, largely because they lack the time, resources and capability to do so. This does not mean that they cannot move towards becoming digital businesses. But, as Willcocks et al. (2024) show, it does mean that they will have to do so at a different pace, fashioning their own ‘catch-up’ evolutionary paths. Fundamentally they are playing out an IT/digital balancing act over time.

Unsurprisingly, most businesses are dependent on a massive legacy of existing technologies, and also ways of managing them. Where these technologies and management practices continue to keep the business competitive, they will continue to be maintained, while also being evolved. Thus, the present state of most businesses is that they are moving from left to right in Figure 2 and are not so much in a process of digital transformation as digital evolution. For them it is going to take much longer than three to five years to become digital businesses. Remember that it has taken even DBS bank some 15 years to get to where it is today! For most organisations, then, some quite matured management approaches remain very relevant, and indeed some practices can still be found in ‘leader’ organisations, and many more in ‘follower’ organisations even though they have progressed quite far in their digital journeys (Willcocks et al., 2024).

Shifting Technology Management Practices in the 2020s

Most businesses, driven by the volatile and unpredictable global business environment they find themselves in, have been shifting towards being more adaptive, resilient, and responsive. They also recognise their increasing reliance on information, communication and digital technologies and potentially AI. They also know that they need to maintain some level of stability and reliability in structures, processes core labour, systems, data architecture, technology base and culture. The central management problem is how to control and innovate at the same time.

One area we have seen technology management advances in during the 2021–2026 period is leadership roles. The CEO has become much more involved in the technology side of the business and how it is imbedded into business strategy, transformation and operations. The CIO role has often been expanded to cover moving further right in Figure 2 or more often the role of Chief Transformation Officer emerges, staffed by someone from the business side who is responsible for the digital transformation programme. This role will be supported by business line managers e.g., marketing, HR, production, who will be responsible for transformation activities and delivering business value from them. The CIO role may also be split into three with the CIO focusing on improving the inner workings of the company with technology (core systems infrastructure, architecture, including cloud). Meanwhile the Chief Technology Officer (CTO) will typically work on improving the technology that services the customer, that touch the customer directly. Some organisations have a Chief Digital Officer (CDT) that will co-lead any digital transformation while creating new digital experiences and AI-enables solutions. Large companies will also have a Chief Data Officer (CDO) to bring more structure around how they manage and exploit the data assets of the business.

In practice all senior business leaders, and not just the C-suite level, have had to become much more tech-savvy. At the same time international businesses have been pushing tech talent increasingly into the business lines that utilise the technologies and systems. Increasingly the IT function tends to keep top tech talent in-house rather than it being outsourced. Lamarre, Smaje et al., (2026) suggest that the better organisations seem to be moving from a traditional tech talent pyramid consisting of lower skilled staff (70 percent) and experts and competents (30 percent) to a tech talent diamond shape model that reverses these percentages. Small teams of high performers are preferred to large numbers of less productive lower skilled staff.

Existing IT infrastructures are being reconfigured over time as are enterprise IT architectures as businesses adopt more digital platforms, rethink their data architectures, re-organise their data, and re-engineer their operating models. All this is very challenging indeed.

Take platforms. You can build an internal platform to make available internal digital capabilities across the enterprise; a customer-facing business platform; a multi-sided market place platform e.g., Uber, Amazon Marketplace. There are also capability-as-a service platforms allowing others to access a specialised capability e.g., payments and Stripe. But clearly such platforms are not just pieces of technology but require a different way of organising teams, technology and data in order to build them as organisational capabilities.

Data organisation has been a perennial challenge, often ignored as too messy and costly to deal with. This needs a coherent data architecture as a basis for a data platform that can store, process and transform data fast and at scale. This is a major undertaking in most businesses, and still not properly accomplished in many, thus limiting their capacity to operate digitally. Organisations then need to organise for data. (Lamarre, Smaje et al., 2026).

Every business has an operational model. An operating model outlines how the business delivers value to its customers, operates on a day-to-day basis, and achieves its strategic objectives. It focuses on execution. To operationalise their IT, organisations need to align with the pre-existing operational model in the wider organisation. While this achieves a good fit with the organisation at large, this can delay the process of digital transformation, and, according to Krivkovich Lodovico, Weddle et. al., (2026) executives found that a more distributed type of model is more effective for addressing key trends today. When it comes to deployment of new technologies and speed, the distributed model has proved to be superior. According to Lamarre, Smaje et al., (2025) this is because over the last decade or more:

- • technology architecture has become more modular—powered by cloud, APIs and modern data platforms. It becomes easier to assemble and reuse components;

- • contemporary software engineering practices such as agile and DevOps (integrating development and operations in a single process to deliver software) have greatly shortened the cycle between a business need and the technical solution.

Conclusion: The IT/Digital Balancing Act

Since the late 1980s there have been constant calls for IT to become more aligned and in a dialectical relationship with the business—its strategic imperatives, operational models and culture. While some digital leaders, like DBS bank, exhibit these qualities, all too many businesses, even in the mid-2020s, do not. The challenge has been that new technologies arrive and pull their management practices in one direction while their business operational models, and the maintenance and continuing business value of their technologies and systems-in-use all too often pull those management practices in another direction altogether.

Today’s businesses do have to shift towards becoming much more digital. As organisations like DBS bank have demonstrated, it is where superior business value and competitiveness lie in the Convergence/AI centric era they find themselves in. Most organisations will need to take a pragmatic approach rather than attempt big-bang digital transformation. It is important not to run too far ahead of the main business functions and processes, nor lag too far behind.

Note: This article is adapted from Willcocks, L. (2026) Global Business: Management that will be published in August by SB Publishing.

References